Six things you should know about Correspondent Banking

10 May 2021

- Usually a bank providing services to another bank on cross-border basis

- “Correspondent relationship” (and role of the “Respondent”) is defined in EU’s 4th (and now 5th) AML Directive

- Correspondent banks are a related subset. Respondent and Correspondent relationships in EU AML directives do not have to be between banks

- The Correspondent bank is typically a member of one or more ‘clearing’ systems in the destination country (or has a relationship with a direct clearing member which enables them to provide a clearing service indirectly)

- Correspondent banks can (i) hold deposits; (ii) perform FX; (iii) handle trade finance transactions such as Letters of Credit and documentary collections; (iv) complete ‘wire’ transfers, i.e. SWIFT payments; and (v) perform other clearing including international cheques, local ACH, etc.

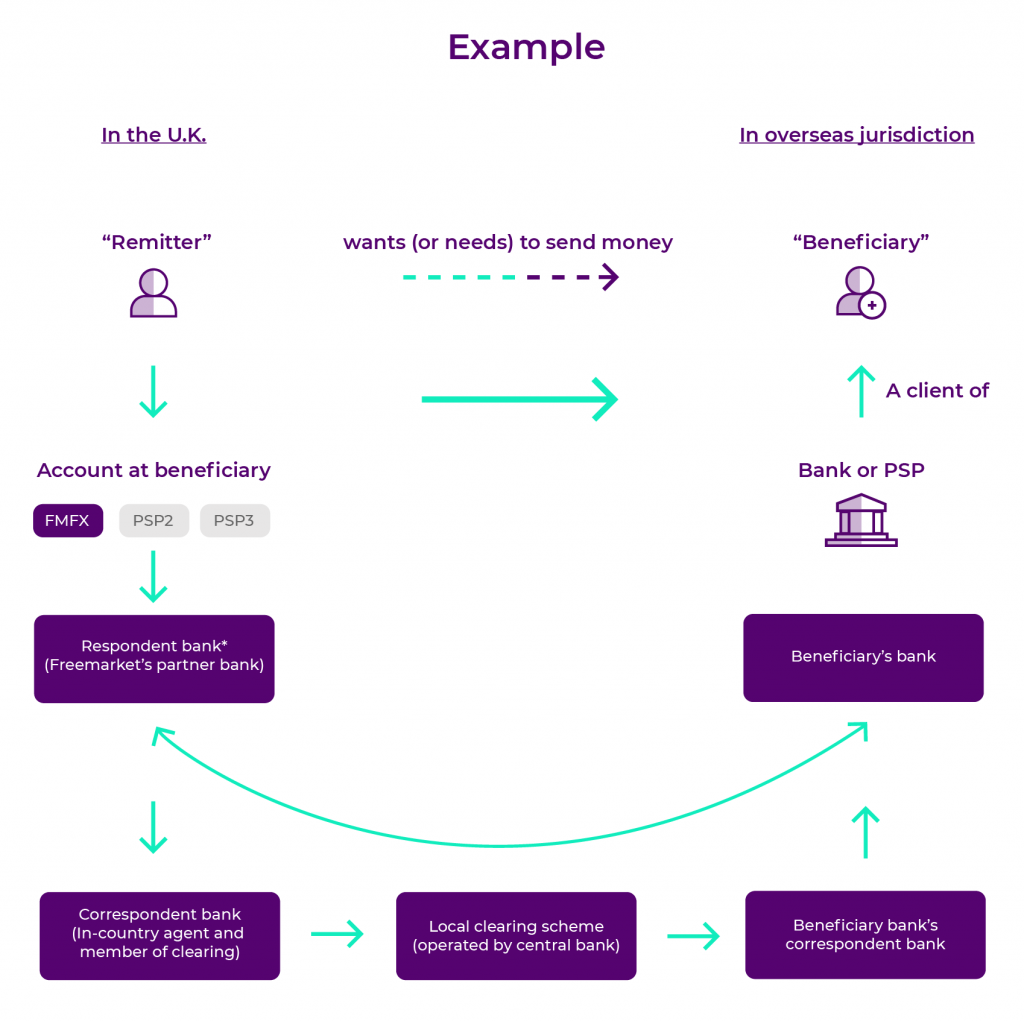

Note that the respondent bank at the start of the chain is the respondent with respect to its Correspondent bank. However, with respect to Freemarket, it has a correspondent relationship for the purposes of AML regulation. In that same context, Freemarket is the Respondent.

How the flow of funds work in Correspondent Banking

When Freemarket’s partner bank receives another currency, say USD, it may not be able to hold those funds itself. The funds will be held as a deposit at their Correspondent bank.

If they are able to hold USD funds themselves (by virtue of membership of one of the USD clearing systems) they are undertaking ‘self-clearing’. In this case, the Respondent bank and the Correspondent banks are the same (although maybe different subsidiaries under the parent entity/within the same banking group).

Nostro account (or is it a vostro?)

The Correspondent bank holds funds in an on-demand deposit account which is generally for the provision of clearing services. The Respondent will have multiple accounts at various banks for different currencies and will refer to these accounts as their ‘nostro’ accounts. ‘Nostro’ is derived from the Latin for ‘ours’.

The Correspondent provides clearing deposit accounts to multiple banks and Financial Institutions for the purpose of access to clearing. The Correspondent refers to the product suite as ‘vostro’ accounts. Vostro is derived from the Latin for ‘yours’.

Nostro and Vostro accounts are the same product. Terminology use depends on whose perspective is taken – the account user or the account provider. This perspective-based approach to naming products is not uncommon in banks; one party’s deposit is another party’s loan.

Safeguarding overlay in Correspondent Banking

The provision of safeguarding from Freemarket’s partner bank to Freemarket remains intact despite the fact that the partner bank does not self-clear, so has to store those funds with their Correspondent.

As with any other deposit, the deposit balance is owed from the partner bank to the depositor (and beneficial ownership vests with the Payment Services User). If the Correspondent holding the funds for the partner bank were to go into liquidation, the partner bank still owes those funds to Freemarket and its underlying clients.

The partner bank will be required to mark and monitor the utilisation of wholesale market credit limits. These limits restrict how much money they are allowed to deposit with other financial institutions, including their correspondents. This limits the potential loss that they can face and underlines that the liquidation of their correspondent would be their issue, not a loss they can pass back up the line to Freemarket or its customers.

Similarly, once the funds have been delivered to the beneficiary’s bank (or PSP), safeguarding is no longer owed. The funds will have actually gone to the beneficiary bank’s correspondent, held for the beneficiary in the beneficiary bank’s nostro account. That is the final leg in the flow of funds.

How clearing works in Correspondent Banking

Clearing generally means the process of confirming, documenting and settling a trade in equities, commodities, etc. as well as managing credit and collateral exposures and supporting monitoring and reporting processes. These processes are handled by a clearing house as they require a single, central, trusted entity that can trade with all its members on terms that enable certainty and consistency.

Central banks typically perform the function of a clearing house for payments., This means they run accounts for, and hold balances deposited by, the local commercial banks (clearing banks). They ensure each is funded and has the requisite capital to protect the financial system in the country and prevent failure. Some central banks also enable the operation of payment systems and payment schemes (e.g. Fedwire in the USA, and various schemes in the Eurozone).

Funds flow in and out of the clearing banks’ accounts at the central bank. The account balances can rise and fall either on a periodic net basis (so the balance changes only by the net amount paid in or out since the last netting operation), or on a gross basis (whereby the balance changes straight away by the whole amount).

Serial vs. non-serial (direct & cover)

For cross-border payments, banks will typically use one of two methodologies for instruction and settlement; one described as ‘serial’, the other as non-serial, or ‘direct and cover’.

In the serial process, only one wire (SWIFT MT103) message is sent from the partner bank to its Correspondent bank. This instructs the Correspondent bank to notify the beneficiary bank and all banks in the chain that a payment is en route to the beneficiary and also creates a process to fund that payment by means of a debit to the Correspondent bank Nostro account.

In the non-serial process, two messages are created at the outset; the MT103 is sent from the partner bank directly to the beneficiary bank, advising that funds are inbound, but it does not also create the funding process. A second SWIFT message (an MT202COV, which copies details from the MT103) is sent from the partner bank to its Correspondent bank, instructing it to send settlement (or place ‘cover’) to the beneficiary bank. The second message is called a ‘cover’ so the whole process is known as ‘direct and cover’.

There are a number of advantages to the non-serial payment process. First, it enables transfers into countries with currency controls. The partner bank is, therefore, able to use existing onshore relationships to source funds for the payment, rather than having to move the funds in from offshore. Secondly, it removes the opportunity for intermediary banks to deduct fees from the principal amount (as they are not handling the MT103 instruction), so the original payment sum can be preserved.

However, the big drawback of non-serial payment processes, and the reason its use has decreased in non-financial counterparty transactions, is that banks have to maintain a huge number of SWIFT network relationships to make it work, rather than just maintaining a single Correspondent bank relationship for each currency. There is significant overhead in maintaining a large number of banking relationships, including the completion of Enhanced Due Diligence on each counterparty bank and the maintenance of bilateral SWIFT authentication keys The additional cost this incurs means that the direct and cover process is not always offered by banks/partner banks. Local Automated Clearing House (Local ACH) vs. Real-time Gross Settlement (RTGS).

Local ACH clearing is typically cheap, often has size limitations that limit the utility of the process and are undertaken on a net basis. Even where they are ‘faster payments’ or ‘instant’ they may have caveats around the target delivery timings so may not have the certainty required of urgent transactions. Consumers might send funds for a birthday present, but wouldn’t typically use it to pay for a house. In the UK, the local ACH is/are Faster Payments and BACS. In Europe, the local ACH is SEPA Credit Transfer (and to a lesser extent SEPA Instant has some utility as the instant payment mechanism).

Real-time Gross Settlement (RTGS) is for payments that are large and/or urgent. They do not wait for netting to take place in a payment system – the whole amount is moved between the accounts held for the relevant clearing banks at the clearing house (or central bank). Funds move rapidly and with little friction. Costs are typically high because these payments require the clearing bank to run a balance (or have a credit facility with the central bank) that can accommodate any transaction size. In the UK, the RTGS system is CHAPS. In Europe, the RTGS system is TARGET2.